Top 10 Mistakes British Expats Make with Their Finances

1. Failing to Plan for Currency Exchange Risks

When you’re earning in one currency and spending in another, exchange rate fluctuations can have a significant impact on your finances.

Many expats overlook this and lose money unnecessarily.

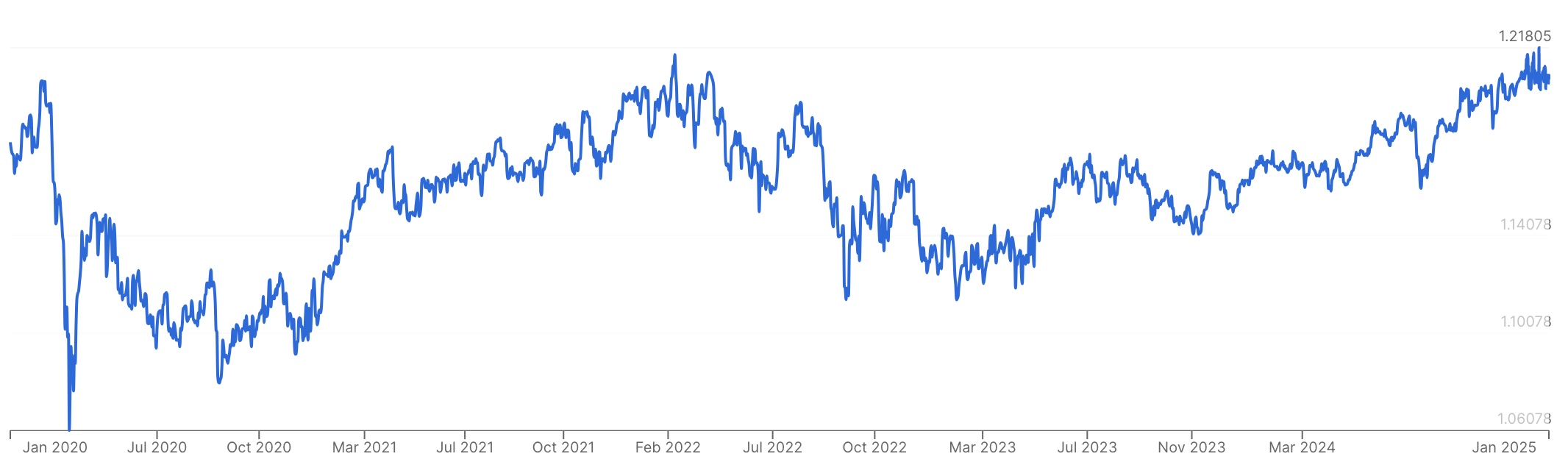

5 Year GBP/EUR

Source: www.xe.com

How to Avoid: Consider using a multi-currency bank account or a specialist foreign exchange service to manage your transfers.

Hedging strategies, such as forward contracts, can also provide stability.

Further Reading:

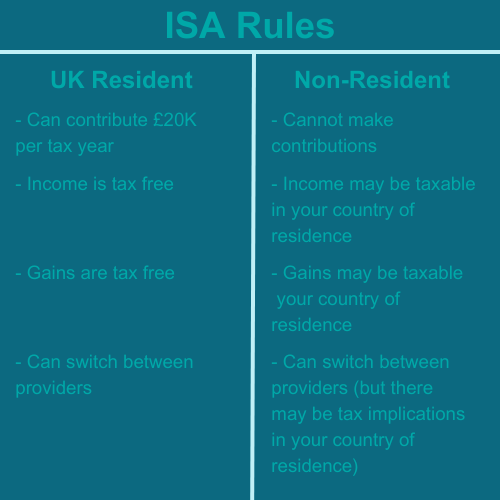

5. Keeping ISAs Without Understanding Restrictions

ISAs are a popular savings vehicle in the UK, but they become less effective when you’re no longer a UK resident.

Contributions are not allowed, and the tax benefits may no longer apply.

How to Avoid: Review your investment portfolio with a financial adviser who understands expat needs.

Alternative tax-efficient investment options may be available in your new country.

ISA Rules:

Case Study 1: Tom and Susan’s Financial Challenges in Saudi Arabia

Tom and Susan moved from the UK to Saudi Arabia 12 months ago with their two young children.

They plan to stay in Saudi for another four years before returning home so their children can attend secondary school in the UK.

Their Financial Goals:

Tom and Susan earn significantly more in Saudi Arabia than they did in the UK.

They want to take advantage of this opportunity to build long-term wealth, ensuring their income is invested sensibly and cost-effectively while also planning for their eventual return to the UK.

The Mistakes They Made:

- Currency Exchange Risks: Tom’s salary is paid in Saudi riyals, but their UK mortgage payments are in pounds. They neglected to use a hedging strategy, losing £5,000 over the year due to unfavorable exchange rates.

- Ignoring Tax Implications: The couple didn’t realize they were still liable for UK tax on their rental income from their UK property. They now face penalties for late filings.

- Estate Planning Neglect: Tom and Susan didn’t update their wills to reflect Saudi inheritance laws, which could create complications for their children if the worst happens.

- Lack of Investment Strategy: While they saved a substantial amount of their income, they failed to invest it effectively. Their funds sat in low-interest accounts, losing value due to inflation.

The Solution:

After realising these mistakes, Tom and Susan sought advice from an expat financial adviser.

Here’s what they did:

- Currency Management: They opened a multi-currency account and used forward contracts to stabilize their mortgage payments.

- Tax Compliance: They worked with a tax adviser to declare their UK rental income and avoid future penalties.

- Estate Planning: They updated their wills to align with Saudi and UK laws, ensuring their children’s inheritance is protected.

- Investment Planning: They implemented a low-cost, diversified investment strategy tailored to their financial goals and time horizon. This allowed their savings to grow while mitigating risks.

- Forward Planning: They created a strategy to lock in the tax efficiency of their investments before returning to the UK.

The Outcome:

With proper financial planning, Tom and Susan maximised their higher income in Saudi Arabia, avoided unnecessary financial losses, and secured a strong foundation for their family’s future.

They now have a clear investment plan, are compliant with tax laws, and are confident about their eventual return to the UK.

Case Study 2: Stuart and Maria’s Retirement in Spain

Stuart and Maria are in their early 60s.

Stuart is British, and Maria is Spanish.

They have three adult children who no longer live in the UK.

They are moving to Spain to spend their retirement years in a country with better weather and a more relaxed lifestyle.

Their Financial Goals:

Stuart and Maria want to ensure their finances are structured for a comfortable retirement in Spain.

They aim to minimise taxes, secure their estate for their children, and adjust their investment portfolio for long-term stability and growth.

They also want to maximise the benefits of their UK pensions while navigating Spain’s tax rules.

The Mistakes They Made:

- Tax Implications: Stuart and Maria initially didn’t understand the Spanish tax system, particularly the wealth tax and how foreign income is taxed. They risked paying unnecessary taxes on their UK pensions and savings.

- Estate Planning: The couple did not update their wills to account for Spanish inheritance laws, which follow forced heirship rules that differ significantly from the UK system. This created potential conflicts for their children’s inheritance.

- Investment Strategy: Their UK-centric investment portfolio was not optimised for their new tax residency in Spain, leading to inefficiencies and unnecessary tax liabilities.

- Currency Exchange Risks: With their UK pensions paid in pounds, they faced significant fluctuations when converting their income into euros for daily expenses.

The Solution:

To address these issues, Stuart and Maria worked with a cross-border financial adviser who guided them through the following steps:

- Tax Planning: They drew the maximum Pension Commencement Lump Sum from their UK pensions before leaving the UK so that these funds would be tax-free (they would have been taxable had they been drawn while resident in Spain). They also made sure that they sold their UK property before becoming tax resident in Spain.

- Pension Review: Stuart considered transferring his UK pensions to a QROPS. However, having discussed the pros and cons with his adviser, he decided that using an international SIPP would be a better solution.

- Estate Planning: They updated their wills to align with Spanish inheritance laws while safeguarding their children’s inheritance rights.

- Investment Optimization: They restructured their investment portfolio using a Spanish-compliant investment bond, which is highly beneficial for residents of Spain.

- Currency Management: They set up a multi-currency account and used a currency broker to lock in favourable exchange rates, ensuring more stable income conversion.

The Outcome:

By taking these steps, Stuart and Maria significantly reduced their tax liabilities, protected their estate for their children, and optimised their investment portfolio for their retirement in Spain.

They now enjoy a financially secure and relaxed lifestyle, with confidence that their long-term goals are well supported.

Talk to an Expert

British expats often face unique financial challenges — from complex tax residency rules to unsuitable offshore investments, frozen pensions, unexpected fees and currency risks. Many of the most common mistakes are avoidable with the right guidance.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping British expats make better decisions with their pensions, savings and long-term financial planning.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

If you’re concerned about high-fee products, poor past advice, unregulated offshore plans, unclear tax exposure, or whether your pensions and investments are still suitable for your expat life, I can help you review your position and identify practical steps to improve it.

Book a confidential consultation