When Bad Advice Costs Everything: How British Expats Can Learn From an England Manager

Talk to an Expert

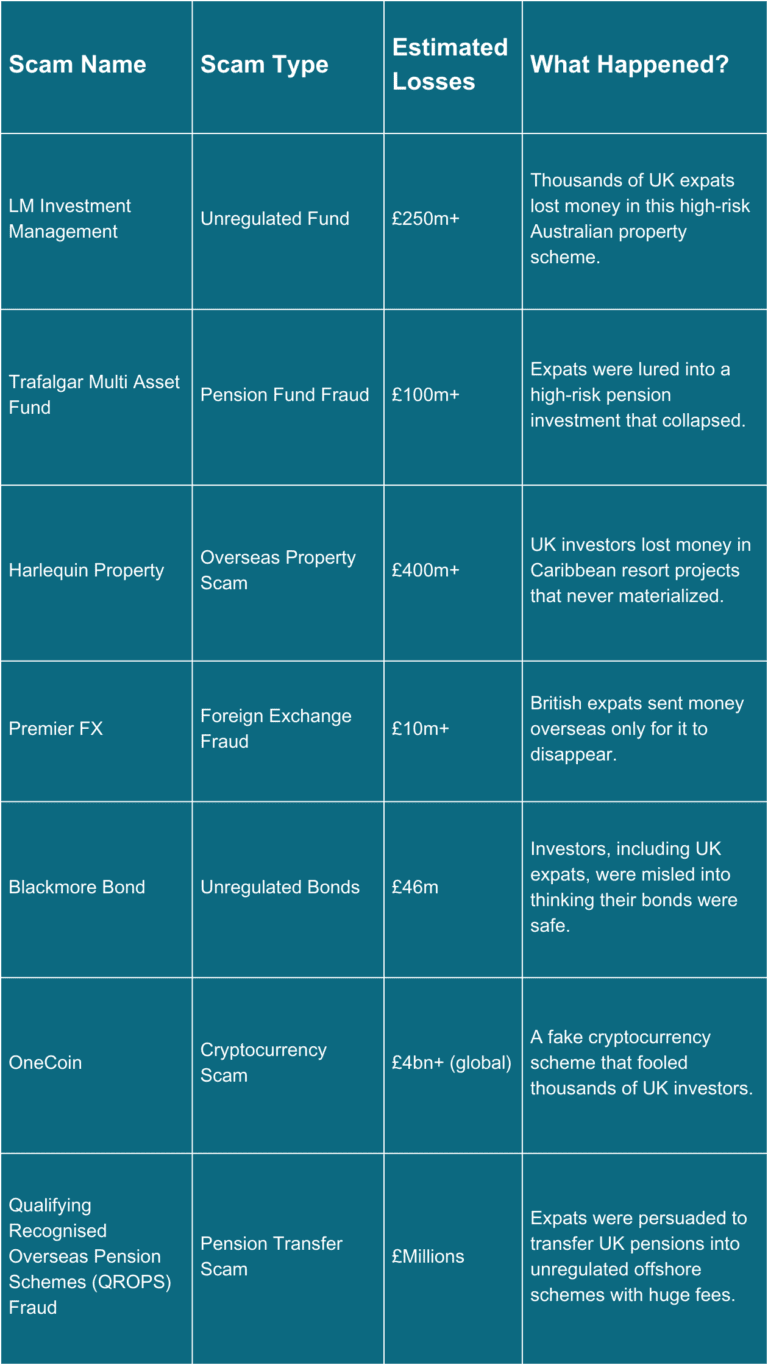

Bad financial advice can destroy decades of hard work — something even high-profile figures, including former England managers, have painfully learned. For British expats, the risk is even greater: offshore salespeople, opaque products, hidden fees and unsuitable investments are far too common.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping expats protect their wealth, unwind bad advice and rebuild with transparent, low-cost, long-term planning.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re concerned about offshore bonds, structured notes, high-fee investment plans, pension transfers, or advice that “sounds too good to be true”, I’ll help you understand what’s right, what’s risky, and what needs fixing — before small issues turn into expensive disasters.

Book a confidential consultation