The danger of home country bias and how to avoid it

Talk to an Expert

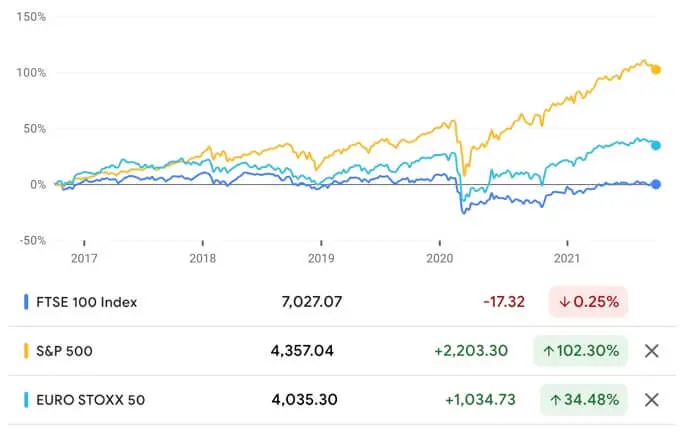

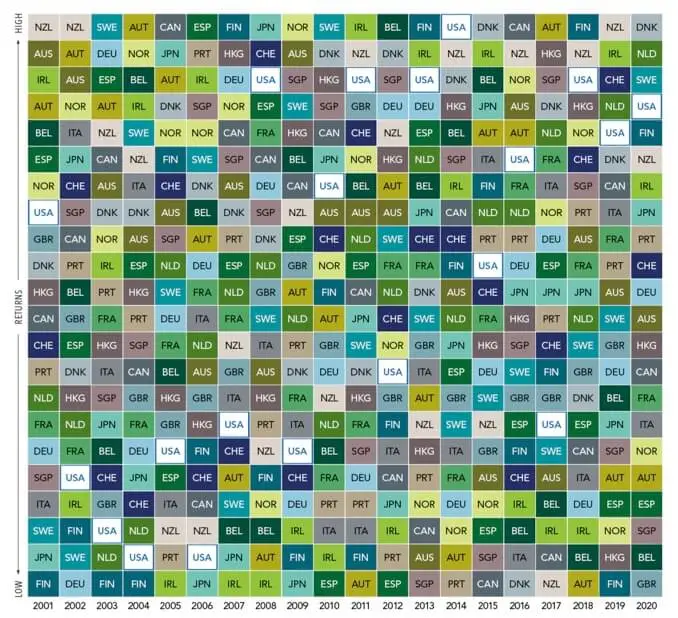

Home country bias is one of the most common – and costly – investment habits. Holding too much in one country’s shares, property or currency can quietly increase risk, especially if you’re a British expat whose life and future spending may be spread across more than one country.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping clients and expats move from unbalanced, home-biased portfolios to globally diversified, evidence-based investment strategies that better match how and where they actually live.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re wondering if you hold too much in UK assets, how to balance UK and overseas markets, how currency risk fits in, or how to diversify without losing sight of your goals, I’ll help you build a calm, rational investment plan that isn’t over-exposed to any single country – including your own.

Book a confidential consultation