Pension Planning Essentials: Why FP2016 and IP2016 Still Matter

With the abolition of the lifetime allowance (LTA) tax charges in April 2024, many individuals assume that they no longer need to worry about pension protections.

However, there are still two forms of transitional protection available that can offer significant benefits: Fixed Protection 2016 (FP2016) and Individual Protection 2016 (IP2016).

Both of these protections offer valuable safeguards, but understanding which one suits your specific circumstances is critical.

This guide will help clarify the differences between the two protections and how you can ensure you’re maximising your pension benefits.

The Deadline is Approaching

Before diving into the details, it’s important to note that the deadline for applying for either Fixed Protection 2016 or Individual Protection 2016 is 5 April 2025.

If you haven’t already applied and are eligible, it’s crucial to act soon to secure the benefits these protections provide.

Why Do You Still Need Protection?

Although the lifetime allowance tax charges were removed in April 2023 and the LTA itself was abolished in 2024, these protections still serve a purpose.

Applying for FP2016 or IP2016 can allow you to secure a higher lump sum allowance (LSA) and lump sum and death benefit allowance (LSDBA) than the standard allowances.

These allowances limit the amount of tax-free lump sums that can be withdrawn during your lifetime and on death.

For those with sizable pension pots, the higher allowances offered by these protections can provide significant tax benefits.

So, which protection is right for you? Let’s take a look at both options.

Fixed Protection 2016 (FP2016)

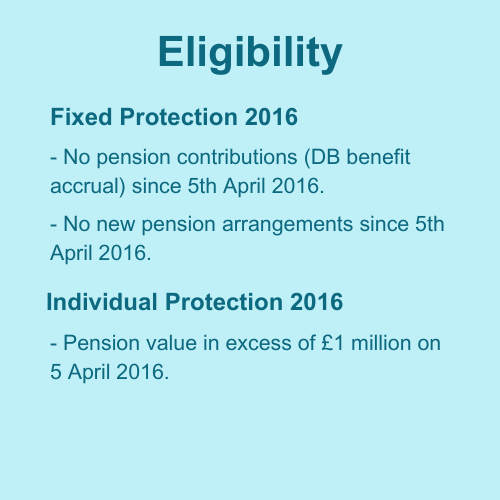

Fixed Protection 2016 is available to those who did not have enhanced protection, primary protection, or a previous version of fixed protection before April 2016.

It doesn’t matter how large your pension pot is now – FP2016 will lock in a lump sum and death benefit allowance based on a specific value.

Benefits of FP2016:

- Maximum Lump Sum Allowance (LSA): £312,500 (vs. £268,275)

- Lump Sum and Death Benefit Allowance (LSDBA): £1.25 million (vs. £1,073,100)

However, there are conditions. If any of the following have occurred after 5 April 2016, you will not be eligible for FP2016:

- You have made further pension contributions, or there has been any benefit accrual under a defined benefit (DB) pension scheme.

- You have started a new pension arrangement (except to accept a transfer of existing pension rights).

It’s important to note that those who had registered for fixed protection by 15 March 2023 have since been able to recommence pension funding or start new arrangements without losing their protection.

However, these rules don’t apply if you missed the earlier registration deadline.

Individual Protection 2016 (IP2016)

Unlike Fixed Protection, Individual Protection 2016 is available to those whose pension benefits were valued at over £1 million on 5 April 2016.

If your pension pot exceeded that threshold at that time, you may be eligible to apply for IP2016.

Benefits of IP2016:

- Lump Sum and Death Benefit Allowance (LSDBA): The value of your benefits as at 5 April 2016, capped at £1.25 million.

- Lump Sum Allowance (LSA): 25% of the LSDBA.

One of the key advantages of IP2016 is that there has never been a requirement to stop pension contributions or accruing benefits under defined benefit schemes, making it a more flexible option for many people.

However, it is only worth applying if the value of your benefits as of April 2016 was higher than the current standard LSDBA of £1,073,100.

Fixed Protection 2016, Individual Protection 2016 and the Overseas Transfer Allowance

The Overseas Transfer Allowance (OTA) limits how much can be transferred to a QROPS without an additional tax charge to £1,073,100 (i.e. the LSDBA).

Anything above this amount will be taxed at 25%.

E.g. you transfer a SIPP worth £1,300,000 to a QROPS, you will be £226,900 over the limit.

£226,900 at 25% means a £56,725 tax charge.

However, if you qualify for either FP2016 or IP2016, you can potentially increase the amount that can be transferred to a QROPS without being hit by the 25% tax charge to £1,250,000.

Transferring A UK Pension Overseas: Why It Pays to Know Your OTA from Your OTC

Can You Apply for Both?

If you’re eligible for both protections, it may be worth applying for both as a belt and braces approach.

In this case, FP2016 would serve as your default protection. However, should FP2016 be lost, IP2016 could then act as a fallback.

Even if your full pension is protected under IP2016 alone, there is still value in applying for both.

For instance, IP2016 could potentially be reduced or lost if your pension benefits are shared on divorce.

By applying for both protections, you ensure that you are covered in multiple scenarios and can protect your pension benefits to the fullest extent.

Case Study 1: Maximising the Lump Sum Allowance (LSA)

Background:

John is 60 years old and has a pension pot valued at £1.5 million.

He’s approaching retirement and planning to start drawing on his pension in the next few years. John’s pension benefits were valued at over £1 million on 5 April 2016, making him eligible for Individual Protection 2016 (IP2016).

John knows that the standard lump sum allowance (LSA), which determines the maximum tax-free amount he can withdraw from his pension, is currently capped at £268,275.

However, if he applies for IP2016, his lump sum allowance could be significantly higher.

The Problem:

Without IP2016, John would be limited to the standard LSA of £268,275, meaning that any additional withdrawals from his pension would be taxed at his marginal rate, increasing his overall tax liability and reducing the amount he can enjoy in retirement.

The Solution:

By applying for Individual Protection 2016, John’s lump sum allowance is recalculated as 25% of the value of his pension on 5 April 2016.

Since his pension was valued at £1.2 million at that time, his new lump sum allowance (LSA) would be £300,000.

This higher tax-free amount allows John to withdraw an additional £31,725 tax-free, compared to the standard allowance.

This reduction in tax liability provides John with more flexibility in managing his finances in retirement.

How to Apply for Fixed Protection 2016

The process for applying for FP2016 is relatively straightforward, as no valuations or detailed benefit information are required. You simply need to confirm that, as of 6 April 2016:

- You were a member of a registered pension scheme (or a relieved member of a non-UK pension scheme).

- You did not have enhanced protection, primary protection, or an earlier version of fixed protection.

- Since 6 April 2016, no event has occurred that would make you ineligible for fixed protection, such as making further pension contributions or accruing benefits.

To apply, you will need to access the process online through the Government Gateway system. It’s important to note that a Government Gateway account is required to submit your application.

Case Study 2: Protecting the Lump Sum Death Benefit Allowance (LSDBA)

Background:

Sarah, a 58-year-old widow, has a SIPP valued at £1.25 million.

She is concerned about the tax implications for her children when they inherit her pension after her death.

The standard lump sum death benefit allowance (LSDBA) is currently set at £1,073,100, which would mean a significant portion of Sarah’s pension could be subject to taxation upon her passing before the age of 75.

Sarah’s pension benefits were valued at £1.25 million on 5 April 2016, making her eligible for Fixed Protection 2016 (FP2016).

The Problem:

Without any form of protection, Sarah’s children would face the lump sum death benefit allowance (LSDBA) limit of £1,073,100.

This means that £176,900 of her pension would potentially be taxed when passed on as a lump sum death benefit.

The Solution:

By applying for Fixed Protection 2016 (FP2016), Sarah can secure a higher lump sum death benefit allowance of £1.25 million.

This fully covers the value of her pension, ensuring that her children will not have to pay any tax on the lump sum death benefit should Sarah pass before the age of 75.

How to Apply for Individual Protection 2016

Applying for IP2016 is slightly more involved, as you will need to provide detailed valuations of your pension benefits as of 5 April 2016.

The information required includes:

- The value of any benefits in payment before 6 April 2006.

- The value of any benefits taken between 6 April 2006 and 5 April 2016.

- The value of any benefits not yet taken by 5 April 2016.

- The amount paid to any overseas scheme where UK tax relief was applied.

- The value of any pension benefits shared as a result of divorce since 5 April 2016.

Please note that if a request for an IP2016 valuation was made before 6 April 2020, pension schemes were required to provide that information within three months.

However, scheme trustees and providers are no longer obligated to provide this information after the deadline.

Once again, the application process is handled online via the Government Gateway.

The Bottom Line

Understanding your pension protections is critical, especially as we approach the deadline for FP2016 and IP2016 applications.

These protections can provide you with significant tax benefits and peace of mind, even in the absence of lifetime allowance tax charges.

If you’re unsure about which protection applies to you, or if you need assistance with the application process, I’m here to help.

As a specialist in cross-border retirement planning for mixed-nationality couples and expats, I can guide you through the complexities of these protections and ensure that you’re maximising your retirement savings.

Contact me today to discuss your pension protection options.

Frequently Asked Questions: Fixed & Individual Pension Protection

What is Fixed Protection 2016 (FP2016)?

FP2016 allows you to lock in a higher lump sum allowance and death benefit allowance, provided no further pension contributions or benefit accruals occurred after 5 April 2016.

What is Individual Protection 2016 (IP2016)?

IP2016 is available if your pension pot exceeded £1 million on 5 April 2016. It provides a personalised protection level up to £1.25 million and allows continued contributions.

What are the benefits of FP2016?

FP2016 secures a lump sum allowance of £312,500 and a death benefit allowance of £1.25 million. However, it requires no pension contributions after 5 April 2016.

What are the benefits of IP2016?

IP2016 allows tax-free lump sums worth 25% of your protected amount, up to £1.25 million, and does not prevent you from making further contributions.

What is the deadline to apply for FP2016 and IP2016?

The deadline for applying for either FP2016 or IP2016 is 5 April 2025.

Can I apply for both FP2016 and IP2016?

Yes, if you’re eligible, you can apply for both. FP2016 serves as default, with IP2016 as a fallback in case FP2016 is lost.

How do these protections affect QROPS transfers?

They can increase your Overseas Transfer Allowance from £1,073,100 to £1.25 million, reducing the 25% tax charge on amounts above the threshold.

How do I apply for FP2016?

You must apply via the Government Gateway and confirm that you haven’t made any disqualifying pension changes since 6 April 2016.

How do I apply for IP2016?

You need to provide detailed valuations of your pension benefits as of 5 April 2016. Applications are submitted online via Government Gateway.

Why is applying for protection still important after the LTA was abolished?

Even without the LTA tax charge, FP2016 and IP2016 offer higher tax-free allowances, which can significantly reduce future tax liabilities on your pension.

Talk to an Expert

Ross is a qualified Chartered Financial Planner and Pension Transfer Specialist.

He has been a cross-border financial adviser for 25 years and specialises in helping British expats manage their finances with clarity and peace of mind.

If you would like to have a no strings chat with him, please get in touch.