Retire to Poland with Confidence: Essential Tips for Brits Looking to Move

Residency & Tax Status: What You Need to Know About Moving to Poland

Residency Rules After Brexit

Since the UK left the EU, British citizens no longer have automatic residency rights in Poland. You must apply for residency via one of the routes below.

1) Residence through a Polish spouse

This is the most straightforward path. If you are married to a Polish citizen, you can apply for a temporary residence card that can lead to permanent residency after a qualifying period.

2) Independent residency

You can also retire to Poland without a Polish spouse by demonstrating that you meet key requirements:

- Proof of regular passive income (e.g., pensions)

- Valid health insurance

- A registered address in Poland

- Clean criminal record

Polish Tax Residency: What It Means

If Poland becomes your centre of vital interests or you otherwise meet residency criteria, you will be treated as a Polish tax resident.

- Your worldwide income becomes taxable in Poland.

- You must declare relevant foreign assets to the Polish tax authorities.

Careful planning helps avoid double taxation and optimises your income structure.

How to Draw Your UK Pension in Poland (and Minimise Tax)

Accessing Your UK Pension in Poland

In the UK, many people use flexi‑access drawdown (FAD) to control how and when they take income.

However, once you move overseas, some UK providers restrict flexible access. Your options may be limited to:

- Buying an annuity

- Taking 100% as a lump sum, which can trigger:

- Likely UK withholding tax, and

- Polish income tax on most or all of the lump sum

UK Pension Taxation in Poland

Poland does not offer a special flat tax regime for foreign pensions (unlike some countries). Pension income is taxed progressively, like regular earned income.

Under the UK–Poland Double Tax Treaty:

- Your UK State Pension is taxable only in Poland when you are Polish tax resident.

- Income from UK private pensions is also taxable only in Poland (UK government service pensions are a separate category and can be taxed in the UK).

Key Tips

Key Tips

- Inform HMRC that you have left the UK using form P85.

- Apply for a UK “No Tax” (NT) tax code so UK providers do not deduct tax at source when Poland has taxing rights.

- Work with a specialist cross‑border financial adviser to structure pension withdrawals tax‑efficiently.

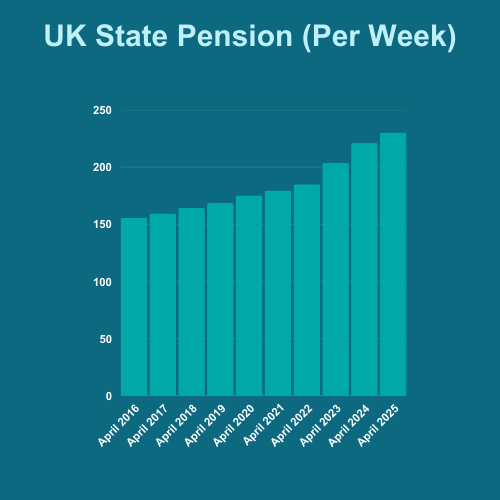

UK State Pension & Poland

The UK State Pension continues to rise annually for residents in Poland under the current reciprocal arrangements. This ensures your State Pension remains protected against inflation while you live in Poland.

Find out more about how the UK State Pension works when you are an expat here

Find out more about how the UK State Pension works when you are an expat here

Thinking of Retiring in Poland?

Download my FREE checklist

Make your move stress‑free with our free Retiring in Poland Checklist. Clear steps, no fluff – just what you need to plan with confidence.

Talk to an Expert

Retiring to Poland from the UK can be a fantastic way to enjoy a lower cost of living, vibrant cities and a high standard of healthcare — but it also raises important questions around tax, pensions, currency and long-term planning.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping British expats in Poland and across Europe align their pensions, savings and investments with local tax rules and long-term retirement plans.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re unsure how your UK pensions and State Pension will be taxed in Poland, how to use the UK–Poland tax treaty, what to do with ISAs and UK property, how to manage currency risk between pounds and złoty, or how Inheritance Tax and estate planning work when you live in Poland, I’ll help you build a clear, confident retirement plan before you make the move — or refine things if you’re already here.

Book a confidential consultation