Thinking of Retiring to Spain from the UK? Here’s What You Need to Know First

Can you still receive your UK pension in Spain?

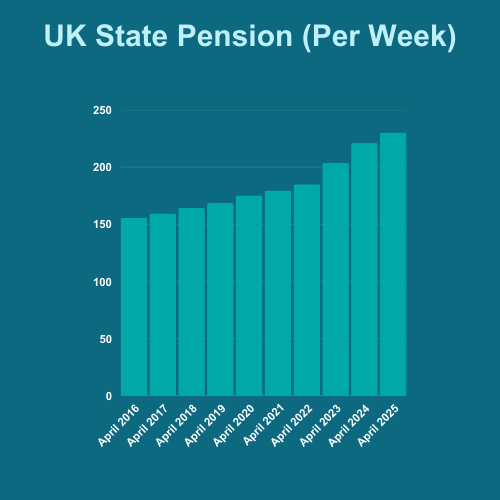

Yes. The UK State Pension can be paid into your Spanish bank account or a UK one.

You’ll continue to receive annual increases (the “triple lock”) in Spain because it’s covered by the UK’s social security arrangements with the EU.

If you have private pensions or SIPPs, these can also be accessed from Spain, but there will be currency risk, tax implications, and paperwork to consider.

In some cases, consolidating UK pensions into an international SIPP or restructuring investments for tax efficiency can make a big difference.

It’s worth seeking advice before drawing pension benefits.

Accessing healthcare in Spain as a UK retiree

Spain has an excellent healthcare system, but access for UK retirees depends on your situation.

If you’re receiving a UK State Pension, you can apply for an S1 certificate from the NHS Overseas Healthcare Service.

This entitles you to state healthcare in Spain, paid for by the UK.

Once registered with the S1 and your local Spanish health centre, you’ll have access to public healthcare on the same basis as Spanish residents.

If you don’t qualify for the S1 (e.g. early retirees), you’ll need private health insurance to cover you, at least until you become eligible for state healthcare.

Thinking of Retiring Overseas?

Download my FREE checklist

Make your move stress‑free with our free Retiring Overseas Checklist. Clear steps, no fluff – just what you need to plan with confidence.

Talk to an Expert

Retiring to Spain from the UK is a dream for many people — but turning that dream into a secure, tax-efficient reality involves far more than just sunshine and property searches. Visas, healthcare, tax residency, pensions, currency risk and Inheritance Tax all need to work together.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping British expats in Spain and across Europe plan their move, structure pensions and investments, and understand the long-term financial implications of living abroad.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re unsure how your UK pensions will be taxed in Spain, how to use the UK–Spain tax treaty, what to do with ISAs and UK property, how currency affects your income, or how to align your estate and IHT planning with a life in Spain, I’ll help you build a clear, realistic retirement plan before you make the move.

Book a confidential consultation