My Big Fat Greek Retirement: A Guide for UK Citizens Looking to Retire to Greece

Residency & Tax Status: What You Need to Know About Retiring in Greece

Since the UK left the EU, UK citizens no longer have automatic residency rights in Greece.

If you’re planning to retire there, you must obtain a residence permit through one of the following routes:

1️⃣ Standard Retirement Visa

This option is available if you can prove sufficient passive income (from pensions, rental income, or investments).

The exact financial requirements can vary, but in general, you should be able to show:

✔️ At least €2,000 per month in passive income (this may be higher for couples).

✔️ Private health insurance coverage.

✔️ A clean criminal record.

2️⃣ The Greek “Golden Visa” – A Fast-Track to Residency

If you’re considering purchasing property, investing €250,000+ in Greek real estate can provide residency for you and your family.

The benefits include:

✔️ Family inclusion – Covers spouses, children under 21, and parents.

✔️ No requirement to live in Greece full-time.

✔️ Schengen Area access – You can travel freely across the EU.

After seven years, Golden Visa holders can apply for Greek citizenship—which, for those considering long-term retirement in Greece, could be a valuable option.

Greek Tax Residency Rules

If you spend more than 183 days per year in Greece, you will be considered a Greek tax resident, meaning:

✔️ You will be liable for tax on worldwide income (unless under a special tax regime).

✔️ You may still be subject to UK inheritance tax (IHT) if you remain UK-domiciled*.

✔️ You must declare foreign assets above €100,000 to Greek tax authorities.

Given the complexity of UK-Greece tax issues, careful financial structuring is essential before relocating.

* From 6th April 2025, the UK is moving to a system based on residence, not domicile.

How to Draw Your UK Pension in Greece (and Minimize Tax)

One of the biggest financial advantages of retiring in Greece is the 7% flat tax rate on foreign pension income.

This regime applies to:

✔️ UK private pensions (SIPPs, QROPS, company pensions).

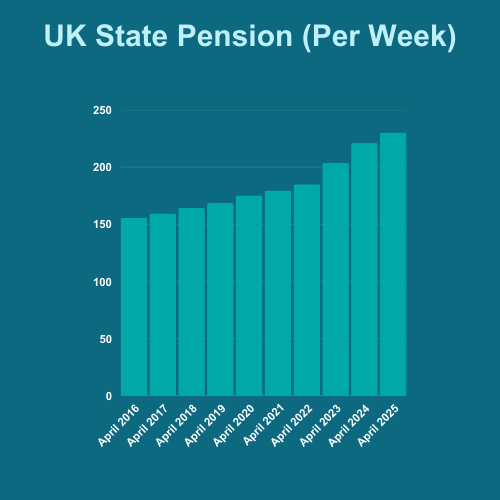

✔️ UK State Pension.

✔️ Annuities and pension-like income from overseas.

Eligibility for the 7% Pension Tax Regime

To qualify for the 7% flat tax rate, you must:

✔️ Have a foreign pension or pension-like income.

✔️ Not have been a Greek tax resident for 5 of the last 6 years.

✔️ Transfer from a country with a tax treaty with Greece (like the UK).

Key Pension Tax Planning Considerations

❗ Take Your UK 25% Pension Lump Sum Before Moving – Once you become a Greek tax resident, your pension withdrawals are taxed at 7%, including your pension commencement lump sum (PCLS).

❗ Plan your pension withdrawals carefully – Work with a cross-border adviser to structure your pension income efficiently.

❗ Apply for a UK “No Tax Code” – This ensures that HMRC does not deduct tax at source from your pension payments.

Thinking of Retiring Overseas?

Download my FREE checklist

Make your move stress‑free with our free Retiring Overseas Checklist. Clear steps, no fluff – just what you need to plan with confidence.

Talk to an Expert

Thinking about retiring to Greece? The lifestyle may be appealing, but before you make the move it is important to understand how your UK pensions, tax position, healthcare arrangements, investments and estate planning could be affected once you become resident overseas.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years' experience helping British expats make confident financial decisions before and after relocating abroad.

Over the years, I have worked with individuals and families retiring across Europe, helping them understand how their pensions, retirement income, tax affairs and long-term financial plans fit together so they can avoid costly mistakes and retire with greater confidence.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you're trying to understand how your UK pensions will be taxed in Greece, how to structure your retirement income, how currency movements could affect your spending power, or how inheritance and succession rules may impact your family, I can help you build a retirement strategy that works across borders and adapts as your circumstances change.

Book a Discovery Call