What Is Specialist Expat Financial Advice and Why Do You Need It?

TL;DR

Specialist expat financial advice focuses on the complex interaction between UK tax, pensions, inheritance rules, and the laws of the country where you live. Standard UK advice often does not account for cross-border residency tests, double tax treaties, offshore structures, or future return planning. Without expertise in expatriate issues, well-intended decisions can create unintended tax and compliance problems. Working with an adviser experienced in expat planning helps ensure your strategy is coordinated across countries and built for the long term.

Looking for Specialist Financial Advice as a British Expat?

Living overseas can make even straightforward financial decisions significantly more complex. Your pensions, investments, tax position and estate planning may all be influenced by the country you now live in, your residency status and how different jurisdictions interact with one another.

Specialist expat financial advice is about looking at the complete picture rather than individual products. By coordinating your retirement planning, investment strategy, tax efficiency and long-term financial goals, you can make decisions with greater confidence while reducing the risk of costly mistakes.

Every British expat’s circumstances are unique. Whether you have recently moved abroad, are planning your retirement overseas or are considering returning to the UK in the future, receiving advice that takes your cross-border financial position into account can provide valuable clarity and peace of mind.

A discovery call gives you the opportunity to discuss your circumstances with an experienced Chartered Financial Planner, understand the options available to you and explore how a personalised financial strategy can support your long-term objectives wherever life takes you.

🌍 Best financial advice for British expats living abroad

Living abroad can be an exciting adventure.

But when it comes to managing your finances as an expat, things can quickly become complex.

Different tax rules, exchange rates, and regulations can make it difficult to know if you’re making the right financial decisions.

For instance, expats often face challenges like double taxation—where the same income is taxed in both the UK and their country of residence—or currency loss due to unfavourable exchange rate movements.

That’s where specialist expat financial advice comes in.

If you’re a British expat, understanding your financial options is essential to protect and grow your wealth.

This blog post will explain what expat financial advice is, why it’s important, and how it can help you navigate the unique challenges of living overseas.

💼 What Is Expat Financial Advice?

Expat financial advice is tailored guidance designed specifically for individuals who live outside their home country.

It involves navigating complex issues such as:

- Cross-border tax rules

- Currency exchange risks

- Local regulations

- Your long-term financial goals (e.g., retirement or inheritance planning)

For British expats, this often means dealing with UK pensions, ISAs, and inheritance tax planning while adhering to the rules of your new country of residence.

Expat financial advice is provided by professionals who understand the complexities of international financial planning and can help you make the most of your money wherever you’re living.

❗ Why Is Expat Financial Advice Important?

Moving abroad doesn’t mean you can leave financial planning behind.

In fact, being an expat often makes financial planning even more crucial. Here’s why:

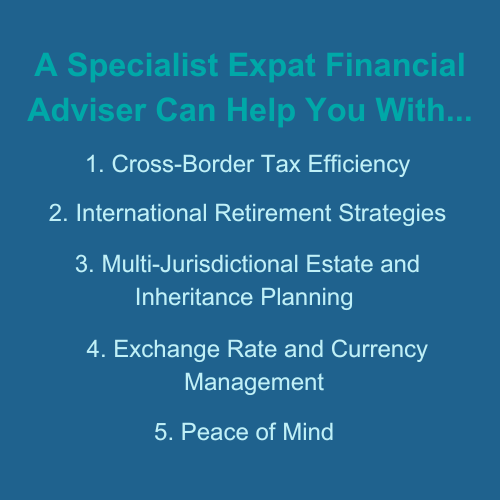

1. Navigating Cross-Border Tax Rules

Tax rules can vary significantly between countries.

For example, your Pension Commencement Lump Sum (PCLS) will be tax-free in the UK. However, if you draw it while resident in Spain, it will be taxed in the same way as other pension income.

In addition, some countries have double tax treaties with the UK, whereas others do not.

Understanding these differences is crucial for effective financial planning.

Expat financial advice helps to ensure that you’re compliant with both UK and local tax laws. It can also help you reduce your tax liability by taking advantage of available reliefs and exemptions.

2. Managing UK Pensions While Living Overseas

Understanding your UK pension options is essential if you’re a British expat.

According to recent data, over 100,000 British expats have transferred their pensions to a QROPS in the past decade, highlighting the popularity of this option.

Similarly, SIPPs remain a widely used choice for expats who prefer to retain UK-based pensions while living overseas.

An expat financial adviser can help you:

- Determine the best pension strategy

- Understand the tax implications

- Plan for drawing your pension income tax-efficiently while living abroad

3. Dealing with Currency Exchange Risks

Living abroad means you’ll likely deal with multiple currencies. Exchange rate fluctuations can have a big impact on your savings, investments, and pension income.

For example, in 2016, the pound sterling dropped by over 15% against the euro following the Brexit referendum, significantly affecting expats who relied on UK pensions or investments for their income.

Expat financial advice can help you:

- Hedge against currency risk

- Choose investments that align with your currency needs

🪦 4. Estate and Inheritance Planning

Inheritance tax rules in the UK can still apply to you.

Even if you’re living overseas, IHT rules may mean that your UK assets remain subject to inheritance tax, making proactive estate planning essential.

For example, a recent case study revealed that a British expat living in Spain faced a significant inheritance tax bill on UK assets, highlighting the importance of proactive estate planning.

An expat financial adviser can help you structure your estate to reduce tax liabilities and ensure your assets are distributed according to your wishes.

📵 5. Limited Access to UK Products

Many UK-based financial advisers won’t work with expats because of regulatory restrictions.

In fact, a recent survey found that over 60% of UK financial advisers avoid working with expats due to compliance challenges and the complexity of cross-border regulations.

Plus, traditional UK financial products, like ISAs, are often inaccessible once you move abroad.

An expat financial adviser understands the products and solutions available to you as a non-resident and can recommend alternatives that meet your needs.

Specialist Advice Covers More Than Individual Financial Products

One of the biggest misconceptions among British expats is that financial planning is simply about selecting the right pension, investment or savings product. In reality, successful financial planning is about ensuring every part of your financial life works together, both now and throughout retirement.

Living overseas often means dealing with multiple tax systems, different legal frameworks and financial rules that may not exist in the UK. Decisions that appear sensible in isolation can have unintended consequences elsewhere, which is why specialist expat financial advice takes a broader, more coordinated approach.

UK Pensions

Your UK pensions may remain one of your most valuable assets after moving abroad. Understanding how workplace pensions, personal pensions, SIPPs and the UK State Pension interact with your country of residence is an essential part of long-term retirement planning. Specialist advice can help ensure your pension strategy continues to support your future objectives while remaining as tax-efficient as possible.

Cross-Border Tax Planning

Tax residency, double taxation agreements and local tax legislation can all influence how your income, investments and pensions are taxed. A coordinated tax strategy can help reduce unnecessary liabilities while ensuring your financial arrangements remain compliant in both the UK and your country of residence.

Retirement Planning

Retirement planning is about much more than deciding when to stop working. It involves creating a sustainable income strategy that considers inflation, longevity, currency movements, healthcare costs and changing lifestyle needs. Reviewing these factors together helps build greater financial confidence for the years ahead.

Investment Management

Investment decisions should reflect your objectives, tolerance for risk, retirement timescale and international circumstances. Rather than focusing on individual investment products, specialist advice considers how your investments complement your pensions, tax position and long-term financial goals.

Estate Planning

Living abroad can create additional complexities for inheritance planning, succession laws and the distribution of your estate. Reviewing your estate planning alongside your pensions, investments and family circumstances can help ensure your wishes are carried out as intended while reducing potential complications for your beneficiaries.

Returning to the UK

Many British expats eventually return to the UK, whether by choice or because their circumstances change. Planning ahead for a future return can help avoid unexpected tax issues, improve pension planning opportunities and make the transition back to UK financial life considerably smoother.

Effective expat financial planning is about much more than choosing individual financial products. It requires a coordinated strategy that adapts as your circumstances, legislation and long-term objectives change.

🌍 How Can Expat Financial Advice Help You?

Here are some specific ways expat financial advice can make your life easier:

🗺️ Creating a Financial Plan

A good adviser will take the time to understand your goals and create a tailored financial plan.

Whether you’re saving for retirement, investing, or planning to buy property, they’ll ensure your plan is realistic and aligned with your lifestyle.

📈 Optimising Your Investments

Expats often face additional challenges when investing, such as dealing with local investment restrictions or currency risk.

A financial adviser can:

- Recommend tax-efficient investment options

- Help you diversify your portfolio across regions and currencies

- Ensure your investments comply with local regulations

🛡️ Protecting Your Wealth

Expat financial advice isn’t just about growing your wealth—it’s about protecting it too.

Advisers can help you manage risks by recommending appropriate insurance, currency hedging strategies, and estate planning solutions.

🧘 Providing Peace of Mind

Perhaps the most significant benefit of expat financial advice is peace of mind.

Knowing that your finances are in good hands allows you to focus on enjoying your life abroad.

🧑💼 What to Look for in an Expat Financial Adviser

If you’re considering working with a financial adviser, here are some things to keep in mind:

🎯 1. Expertise in Expat Financial Planning

Not all financial advisers understand the complexities of expat finances.

Look for someone with experience in cross-border tax, pensions, and investments.

🎓 2. UK Qualifications

A UK-qualified adviser, such as a Chartered Financial Planner, has the credentials to provide high-quality advice.

🔍 3. Transparency

Make sure the adviser is upfront about their fees and any potential conflicts of interest.

Unsure Whether You Need Specialist Expat Financial Advice?

Living overseas can create financial opportunities, but it can also introduce complexities that are easy to overlook. Whether you have recently moved abroad or have been an expat for many years, reviewing your financial position with a specialist adviser can help ensure your plans remain aligned with your long-term goals.

Every expat’s circumstances are different. Your country of residence, tax status, family situation, pensions, investments and future plans all influence the advice that is appropriate for you. A strategy that works well for one British expat may be entirely unsuitable for another.

International finances create additional complexity. Cross-border taxation, multiple pension arrangements, currency considerations and differing legal systems mean that financial planning for expats often requires a broader perspective than traditional UK financial advice.

Planning opportunities can easily be missed. Decisions about pensions, investments, tax residency or estate planning often become more difficult—or more expensive—to change later. Identifying opportunities early can help you avoid unnecessary costs and make better long-term decisions.

Early advice often creates greater flexibility. The sooner your financial affairs are reviewed, the more options you are likely to have. Proactive planning allows you to structure your finances more efficiently while adapting to changes in legislation, residency or personal circumstances as they arise.

Specialist expat financial advice is not simply about solving today’s challenges. It is about building a coordinated financial strategy that supports your lifestyle, protects your wealth and gives you confidence wherever life takes you.

If you’re unsure whether specialist expat financial advice could benefit you, a discovery call is an opportunity to discuss your circumstances, understand your options and explore how a personalised financial plan could help you achieve your long-term objectives.

🤔 Do You Need Expat Financial Advice?

If you’re a British expat or planning to move abroad, professional financial advice can help you:

- Avoid costly mistakes

- Save money on taxes

- Make informed decisions about your pensions and investments

Without proper advice, it’s easy to feel overwhelmed by the complexities of expat life.

A qualified adviser can guide you through the process, giving you confidence that your financial future is secure.ts

Real People, Real Results

“Taxation, pensions, inheritance, capital gains and investing are areas that need qualified and expert advice. I would certainly be lost without him. If you are an expat looking for sound financial advice, then you would do well to reach out to Ross.”

— Malcolm Ridge

❓ Frequently Asked Questions

What is expat financial advice?

Expat financial advice is specialised guidance tailored to individuals living outside their home country. It covers tax planning, investments, pensions, currency issues, and estate planning specific to cross-border situations.

Why do British expats need financial advice?

British expats face complex financial rules, including different tax regimes, pension access issues, and international investment laws. Financial advice ensures they stay compliant and optimise their financial outcomes.

How is expat financial advice different from local advice?

Local advisers may lack experience with UK-specific financial products and regulations. Expat financial advisers understand both UK rules and international requirements, helping clients navigate both jurisdictions effectively.

Can I still use a UK financial adviser if I live abroad?

Yes, but not all UK advisers are qualified or regulated to advise expats. It’s essential to work with someone who understands cross-border regulations and has experience dealing with expats.

What are the main tax issues for British expats?

British expats often face double taxation, different capital gains rules, and exposure to UK inheritance tax. Professional advice helps reduce liabilities and ensure legal compliance.

Can expat advisers help with UK pensions?

Yes. Advisers can help assess whether to keep your UK pension, transfer it to a QROPS, or manage it through a SIPP—while considering tax implications in your country of residence.

Do expats still pay UK inheritance tax?

Yes, UK inheritance tax may still apply if you are considered UK-domiciled. Financial planning can help mitigate IHT exposure through trusts, insurance, and asset structuring.

What’s the typical cost of expat financial advice?

Costs vary based on the adviser’s model. Common options include hourly rates, fixed fees, retainers, or a percentage of assets under management (typically 1% to 1.5%).

Is expat financial advice regulated?

Yes, but regulation depends on the adviser’s location and the services offered. Look for advisers with UK qualifications and cross-border expertise relevant to your residence country.

How do I choose the right expat financial adviser?

Choose someone with experience in expat finances, UK qualifications, and transparent fees. It’s also important they understand your destination country’s tax and legal framework.

Common Financial Planning Mistakes British Expats Make

Moving abroad creates exciting opportunities, but it can also introduce financial complexities that are easy to underestimate. Many British expats continue to make decisions based on UK financial rules without fully considering how living overseas changes the way pensions, investments, taxation and estate planning interact. Avoiding the following common mistakes can help protect your wealth and improve your long-term financial security.

Relying on Advisers Without Expat Expertise

Not every financial adviser understands the additional challenges faced by British expats. Cross-border taxation, international pension rules, double taxation agreements and changing residency regulations require specialist knowledge. Advice that is suitable for someone living permanently in the UK may not deliver the best outcome once you are resident overseas.

Treating Pensions, Investments and Tax Separately

One of the most common mistakes is viewing each financial decision in isolation. Your pensions, investments, tax position and retirement income are closely connected, and a decision in one area can have unintended consequences elsewhere. A coordinated financial plan helps ensure every element works together towards your long-term objectives.

Ignoring Changes in Tax Residency

Your tax obligations can change significantly after moving abroad. Becoming tax resident in another country may affect how your pension income, investments, capital gains and other assets are taxed. Failing to review your tax position regularly can result in missed planning opportunities or unexpected liabilities.

Delaying Financial Reviews After Moving Abroad

Many expats postpone reviewing their financial arrangements until retirement or after a major life event. Unfortunately, delaying action can reduce the number of planning opportunities available. Regular financial reviews allow your strategy to evolve alongside changes in legislation, tax rules and your personal circumstances.

Assuming UK Financial Rules Apply Overseas

Financial legislation differs from one country to another. Pension taxation, inheritance laws, investment regulations and reporting requirements can all vary depending on where you live. Assuming UK rules automatically continue to apply can lead to costly misunderstandings and unnecessary financial risk.

Taking a proactive approach to financial planning can help you identify opportunities before they disappear, reduce unnecessary tax exposure and ensure your financial arrangements remain aligned with your changing lifestyle and future ambitions.

Specialist expat financial advice is about understanding how every part of your financial life works together. A coordinated approach can help you avoid costly mistakes while supporting your long-term financial goals wherever you choose to live.

Whether you have recently moved overseas, have lived abroad for many years or are planning an eventual return to the UK, reviewing your financial strategy with an experienced expat financial adviser can provide greater clarity, confidence and peace of mind for the future.

🧭 Final Thoughts

Expat financial advice is an essential service for anyone living outside their home country.

By working with a trusted adviser who specialises in cross-border finances, you can gain clarity and confidence in your financial future.

Schedule a “no strings” call today to learn how I can help you protect and grow your wealth, no matter where life takes you.

Also Read

Talk to an Expert

Finding the right financial adviser is one of the most important decisions a British expat can make. Living abroad often means dealing with multiple tax systems, different pension rules and financial legislation that spans more than one country. Advice that works well for UK residents may not always be appropriate when your finances are international.

I'm Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years' experience helping British expats worldwide navigate the complexities of cross-border financial planning and build long-term strategies with confidence.

Rather than focusing on individual financial products, I take a holistic approach that brings together your UK pensions, investments, tax planning, retirement income, estate planning and future objectives. Every recommendation is designed to support your wider financial wellbeing, wherever you choose to live.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you're planning your retirement overseas, reviewing your UK pensions, considering your investment strategy or preparing for a future return to the UK, I'll help you understand how every part of your financial life fits together so you can make informed decisions with confidence.

With the right planning, complex international finances become a coordinated long-term strategy rather than a collection of disconnected decisions.

Book a Discovery Call