Independent, UK-qualified pension advice for British expats in or approaching retirement

– because your location shouldn’t limit your retirement options.

Planning your retirement from abroad?

Like many British expats, you face a frustrating reality:

Your UK pension is likely your biggest retirement asset, but trying to access it as a non-resident is harder than it should be.

You may find your pension provider is unhelpful. They may freeze your online access, delay payments, or insist on paper-based instructions. Some refuse to make overseas payments altogether.

UK-based financial advisers often can’t help you, and local advisers in your new country may not understand UK pensions at all.

Your tax situation is suddenly far more complicated than expected.

The result?

Stress, confusion, and sometimes, poor decisions with lifelong consequences.

This is where I come in.

My solution

I offer a specialist Retirement Beyond Borders™ service for people like you.

As a UK Chartered Financial Planner and cross-border retirement specialist, I can help you:

- Understand your pension options

- Access your pension funds flexibly and tax-efficiently

- Navigate HMRC and apply for an NT (No Tax) code where appropriate

- Minimise double taxation risks

- Get proper, transparent, fee-based financial advice, just like you would in the UK

All while making the process clear, calm, and stress-free.

What you get

My service is fully independent and always fee-based — no hidden charges, no commissions, and no product-pushing.

You’ll get:

☑️ Clear, written advice tailored to your circumstances

☑️ A tax-efficient plan for drawing your UK pension overseas

☑️ Support with HMRC processes and paperwork

☑️ Coordination with local advisers or accountants, if needed

👉 Book Your Free Discovery Call

Or download your free checklist below.

Who is this for?

You’re a British expat, either already retired or within a few years of retirement.

You’ve built up pension savings in the UK, often in a personal pension or SIPP, but now live overseas.

And you’re wondering:

- What’s the best way to access my UK pension from abroad?

- What taxes will I pay, both in the UK and in my country of residence?

- How do I get a No Tax code from HMRC?

- Is there a way to draw down my pension flexibly and efficiently?

- How will the proposed changes to the way UK pensions are treated for Inheritance Tax affect me as an expat?

- Can I still get proper, independent financial advice, even as a non-resident?

If that sounds familiar, you’re in the right place.

About Me

I’m Ross Naylor, a UK Chartered Financial Planner with 29 years of experience, and a specialist in cross-border retirement and estate planning.

I’ve lived outside the UK for 24 years myself and understand the emotional and financial complexities of international financial planning.

I created the Retirement Beyond Borders™ service to give expats like you expert guidance, clarity, and peace of mind regarding your pension options.

Common scenarios I help with

- You’re retiring to Spain, Portugal, France, or elsewhere in the EU

- You are ready to start drawing your UK pension and want to make sure it’s tax-efficient

- You want to transfer your pension but need independent advice first

- Your pension provider is making life difficult as a non-resident

- You’ve been told you need an NT code, but don’t know how to get one

- You’re not sure who to trust for advice

Case Study: Steve’s Great Big Expat Pension Problem in Spain

Steve, 62, retired to Spain four years ago, but ran into unexpected problems when trying to access his UK pensions.

Here’s what happened:

- Steve has three personal pensions in the UK, worth a total of £450,000.

- At age 60, he took his full 25% Pension Commencement Lump Sum (PCLS) from each scheme.

- Unfortunately, he and his UK adviser didn’t realise that Spain taxes this lump sum. What was tax-free in the UK turned out to be taxable in Spain.

- When Steve realised the mistake, he tried to find a UK adviser who truly understood expat issues, but came up empty.

Then, things got worse:

- Steve now wanted to start drawing income from his pensions.

- But because he was no longer UK-resident, his pension providers wouldn’t allow flexible drawdown.

- They insisted all instructions be sent by post.

- His only remaining options?

- Buy an annuity (almost impossible to arrange from Spain)

- Or withdraw the whole pension in one go — triggering a huge tax bill in Spain

The Solution: A Flexible, Cross-Border Pension Approach

That’s where we came in.

We helped Steve:

- Transfer his three pensions into an International SIPP

- This gave him full flexi-access drawdown, just like he’d have in the UK

- It also came with a modern online portal — no more sending paperwork by post

- Apply for a No Tax (NT) code from HMRC

- This meant no UK tax was deducted at source

- Steve now only pays tax in Spain, under the rules there — avoiding double taxation

- Create a clear drawdown plan

- We set up a diversified, low-cost investment strategy to support Steve’s long-term goals

- His income is now flexible, tax-efficient, and aligned with his lifestyle in Spain

Where Steve is now

Steve says he finally feels in control of his finances again.

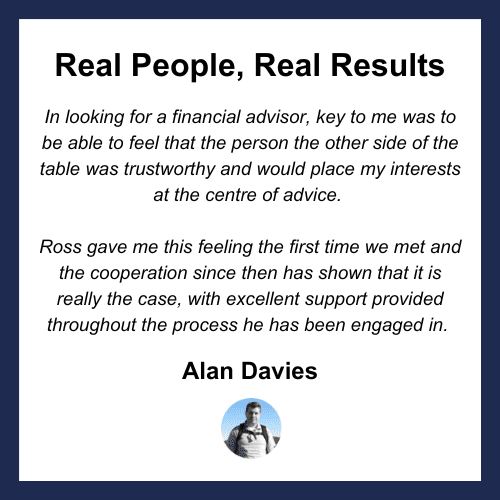

“For the first time since leaving the UK, I actually understand how my pensions work. I’ve got proper access to my money, I’m not overpaying tax, and I’ve got someone who actually gets what it’s like living abroad.”

👉 Be Like Steve – book Your Free Discovery Call

Frequently Asked Questions about Expat Pension Advice

1. Can I still access my UK pension if I live abroad?

Yes, but your options may be more limited. Some providers restrict access for non-residents or won’t allow flexi-access drawdown. That’s why many expats transfer their pensions to a more flexible solution, like an International SIPP.

2. Will I be taxed twice on my UK pension (once in the UK and again in my new country)?

You shouldn’t be, but it depends on whether there’s a tax treaty in place and how your pension is drawn. In many cases, you can apply for a No Tax (NT) code from HMRC, which stops UK tax from being deducted at source.

3. What is an NT code (and do I need one)?

An NT code tells your pension provider not to deduct UK tax from your pension income at source. If you’re living in a country that has a tax treaty with the UK, and your income is taxable only in that country, you may need an NT code.

4. Can I transfer my UK pension if I live overseas?

Yes, and in many cases, it’s the most practical option. Transferring to an International SIPP allows you to keep full control, continue drawing your pension flexibly, and manage everything online.

5. Are UK financial advisers allowed to help expats with their pensions?

Most UK advisers are not set up to advise non-UK residents.

6. What are the tax implications of drawing my UK pension while living abroad?

This depends on your country of residence and how your pension income is classified. Each country has different rules, so I always recommend tailored advice, including coordination with local tax professionals where necessary.

7. Can I still access my tax-free lump sum if I live abroad?

Yes, UK pension rules still allow you to take up to 25% of your pension pot as a lump sum, usually free of UK tax.

However, just because it’s tax-free in the UK doesn’t mean it’s tax-free where you live now.

Many countries (like Spain, France, and Portugal) treat the lump sum as taxable income, so you could face a surprise tax bill if you’re not careful.

That’s why it’s important to get advice before making any withdrawals.

8. Can I still draw my pension flexibly from abroad?

Only if your provider allows it — and many don’t.

If you’re blocked from using flexi-access drawdown with your current pension provider, you should look at transferring your pension to a provider who does allow it.

9. Is it expensive to transfer my pension to an International SIPP?

Not necessarily. There are low-cost, fully transparent platforms available where you’ll know all the fees upfront, and there are no commissions or product charges — just clear, fee-based advice.

Read more about expat pensions

🔗 How do I apply for an NT Code for pension income? An expat guide

🔗 Should I Consolidate My Pensions?

🔗 3 Different Ways to Access Your Pension

🔗 How Much Will You Really Retire On? Decoding Your Pension Statement

🔗 Why UK-Based IFAs Won’t Work with Expats (And What You Can Do)

🔗 The Pros and Cons of a SIPP for Expats

🔗 Unlocking Your Retirement: A Guide to Flexi-access Drawdown Rules

Peace of mind, wherever you are

Wherever you live now, and wherever you plan to retire, my goal is to make your pension work for you, not against you.

❌ No jargon

❌ No fluff

❌ No pressure

Just clear, professional advice tailored to your cross-border life.

Next step

If you’d like to explore whether my Expat Pension Advice service is right for you, click the button below to book a free 30-minute discovery call.

We’ll discuss your situation, your goals, and whether I’m the right person to help.

👉 Book Your Free Discovery Call