Should I accept a Pension Increase Exchange? The pros and cons of PIE offers

Other factors to take into account when considering a pension increase exchange

What exactly are you giving up?

How much are your pension payments going to increase by in retirement assuming you do not accept the PIE offer? RPI? CPI? Is there a cap?

Taxation

A higher starting pension now could possibly push you into a higher tax bracket (e.g. from the 20 per cent to the 40 per cent band). This would reduce the value to you of any PIE uplift.

This would be a particular issue if you are still in some form of paid work and the enhanced pension would be in addition to your wages.

Spouses pension

Accepting this kind of offer is also likely to affect the payouts that your spouse will receive if you die before them.

Therefore, if you are married or in a civil partnership, it is important to consult your partner on their wishes.

Often, a spouse will need to provide their signed consent to such an offer.

Health

If you are in poor health then you might welcome the chance to bring forward some extra pension to enjoy now.

If you are in good health then the inflation protection is potentially more valuable.

Also, if you end up needing expensive care later in retirement you might wish you had stuck with a pension that went on rising through your retirement.

In case of death folder checklist

Download this free checklist to ensure your family has everything they need in case of an emergency

Whether you’ve recently become an expat, are in the process of planning to leave the UK, or have been a long term expat and are now preparing to return home, estate planning is essential. Ask yourself: if something happened to you tomorrow, would your spouse or family know where to find your key financial documents?

Family history of longevity

If you come from a family where previous generations were long-lived then you might think that decades of generous inflation protection is a better option than a higher starting pension but decades of lower increases.

Other assets or sources of income

If this pension in question is your only source of income in retirement then the PIE offer is potentially less attractive.

If you have other pension schemes, sources of income or assets to draw on then taking the risk of greater short term income in return for a relatively lower income in later life may have more merit.

Financial strength of employer backing the scheme

Pies could be especially attractive if you are concerned about the schemes financial strength.

If you are concerned about the status of the employer backing the scheme, then having a higher pension now may well be attractive as you get your value out earlier.

It might also be useful in the event that the scheme were to go insolvent and enter the Pension Protection Fund. In such a scenario, your compensation would be based on the enhanced pension.

Lifetime allowance impact

At the point of retirement, an individual receiving an increase in their pension as a result of a PIE will have a higher initial pension. As a result, a higher proportion of that individuals Lifetime Allowance (LTA) will be used.

The way that the capital value of a defined benefit pension is calculated is by multiplying the initial annual pension payable by a factor (usually 20). The higher the initial pension, the higher the capital value.

Let’s use an example. Mr. Smith is in line for a pension of £45,000 from his final salary scheme. Using a factor of 20, this would give him a capital value of £900,000. This is below the current (2020/2021) LTA of £1,073,100.

Therefore, assuming he has no other pensions, he is within the LTA, even though his pension increases every year with inflation.

However, now he has been offered a PIE, which would give him an annual pension of £58,000 which would be fixed for life.

Using the same factor of 20, he now has a capital value of £1,170,000. This is over the LTA and exposes him to a charge of 25% of 55% of the excess amount.

Impact on LTA protections

Where things get slightly more complicated is if you have certain forms of LTA protection.

In particular, if you have enhanced protection or any of the variants of fixed protection.

The reason for this is that, if benefit accrual is deemed to have occurred under these arrangements, this valuable protection may be lost.

Accepting a PIE offer could be considered as benefit accrual.

It is irreversible?

Once you have signed up to the exchange scheme, you cannot change your mind in future years.

Pension increase exchange case study

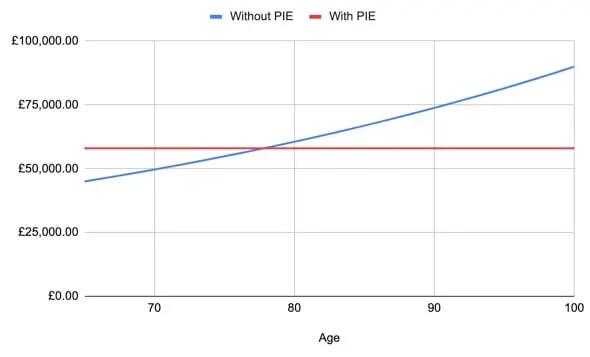

Let’s look at Mr. Smith again, who is in line for a pension of £45,000 from his final salary scheme, with the usual index-linking, but who has been offered the alternative of a £58,000 annual pension that will be fixed for life.

Mr. Smith is 65 years old.

First, let us assume that the Bank of England keeps inflation at its 2 per cent target. (We’ll also assume for simplicity that the CPI and RPI figures are the same – the Bank targets CPI but pensions tend to rise in line with the RPI.)

With inflation at 2pc, it will take a £45,000 pension 14 years to rise to £58,000.

It will take a further 12 years – 26 in total – for Mr. Smith’s total income received to exceed what he would get with a flat rate of £58,000 a year.

If he lives for 30 years, his income will be £81,511 a year. This is £23,511 more than it would be without index-linking.

His total income over 30 years of retirement would be £1,907.074, compared with £1,740,000 if he opted for the fixed £58,000 annual pension.

Higher inflation?

What if the Bank of England fails to meet its target and inflation averages 4 per cent per annum?

Then, it will take a £45,000 pension just seven years to rise above £58,000, and a further six years for the total income received to exceed what he would have got with a flat rate of £58,000 annually.

If he lived for 30 years, his final income would be £177,574 a year – £119,574 more than he would have got without index-linking.

The total income over 30 years of retirement will be £3,391.924, compared with £1,740,000 had he opted for the fixed £58,000 pension.

Talk to an Expert

Pension Increase Exchange (PIE) offers can look tempting: give up some or all of your future inflation-linked increases in return for a higher starting income now. But once you accept, the decision is usually irreversible – and the long-term impact on your security, especially in later life, can be significant.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with nearly 30 years’ experience helping people – including many British expats – weigh up complex defined benefit pension choices such as PIE offers, early retirement options and transfer values.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re unsure how a PIE offer is calculated, how it affects your income in real (inflation-adjusted) terms, what it means for a spouse’s pension, or how it fits with your wider retirement plan, I’ll help you model the trade-offs clearly so you can decide with confidence, not guesswork.

Book a confidential consultation