Retiring Abroad: The Complete UK Expat Guide

Retiring Abroad from the UK

Thinking about retiring abroad from the UK? You’re in good company.

According to the UK’s Department for Work and Pensions, over 1.2 million UK pensioners currently live overseas.

Spain, France, Portugal, Greece, and Poland are among the most popular destinations, each offering its own lifestyle, healthcare system, tax regime, and cost of living.

But while the dream of warm sunshine and lower living costs is appealing, retiring abroad is a complex decision.

Pensions, taxation, property ownership, visas, and healthcare all need to be considered.

This guide is designed as your complete resource, with links to detailed country-specific guides to help you plan confidently.

Why Retire Abroad?

Many British retirees are drawn overseas for a mix of lifestyle, financial, and family reasons.

Top reasons include:

🌞 Better weather – More sunshine and a healthier outdoor lifestyle.

💷 Lower cost of living – Groceries, dining, and utilities are often cheaper than in the UK.

🏡 Property affordability – Attractive home prices compared with southern England.

🍷 Lifestyle and culture – Food, wine, and family-oriented values.

❤️ Family connections – Many Brits marry European spouses and retire to their partner’s country.

📊 Fact: Spain is home to more than 120,000 UK pensioners, France to over 60,000, Portugal’s numbers have grown sharply due to its favourable tax regime, and Poland is one of Europe’s fastest-growing destinations for UK retirees.

Poll

Cost of Living Abroad vs the UK

One of the biggest attractions of retiring abroad is the potential to stretch your pension income further.

- In Portugal, consumer prices are around 25–30% lower than in the UK.

- In Poland, everyday expenses such as transport, food, and healthcare can be 40% lower.

- In Spain, eating out is typically 50% cheaper than in London.

💡 While daily living may be cheaper, imported goods and private healthcare can be more expensive. Always research your intended destination carefully.

UK Pensions Abroad

The UK State Pension

The State Pension is payable worldwide. However, annual increases depend on where you live:

- ✅ EU/EEA, Switzerland, and countries with reciprocal agreements – the State Pension rises each year under the “triple lock”.

- ❌ Countries without agreements (e.g. Canada, Australia, New Zealand, South Africa) – pensions are frozen at the level you first claimed.

This creates significant inequality.

Someone retiring to Spain will see their pension rise each year, while someone in Canada may lose thousands over a 20–30 year retirement.

🔗 Which countries are affected by frozen UK state pension payments? Find out here.

Private Pensions and Lump Sums

Private pensions can be paid abroad, but taxation and drawdown options vary.

- The Pension Commencement Lump Sum (PCLS), often known as the 25% tax-free lump sum, may be taxed in your new country of residence.

- Regular pension income is often taxed where you live, depending on the Double Tax Treaty.

- Some expats explore QROPS (Qualifying Recognised Overseas Pension Schemes), but these are not suitable for everyone.

- Some UK pension providers severely restrict drawdown options for Brits living overseas.

👉 Professional advice before drawing pension benefits is essential.

Tax Considerations

Tax can make or break your retirement plan.

Residency and the Statutory Residence Test

The UK’s Statutory Residence Test determines if you are still a UK tax resident.

This considers:

- How many days you spend in the UK

- Family and work ties

- Whether you own a home in the UK

Once you are non-resident, UK tax may no longer apply to most income, but you will likely become liable for local tax instead.

Double Tax Treaties

The UK has treaties with over 130 countries.

These decide which country taxes your pension and prevent double taxation.

💡 Example: UK pensions are taxable in Spain under the UK–Spain treaty.

No Tax (NT) Codes

When you move abroad and become non-UK resident for tax purposes, you can apply for a No Tax (NT) code from HMRC.

This means:

- Your UK pension can be paid to you without UK tax deducted at source.

- Instead, you are taxed only in your country of residence, in line with the Double Tax Treaty.

💡 Example:

A UK retiree in Spain applies for an NT code. Their pension provider then pays gross (no UK tax deducted), and the pension is taxed in Spain instead. Without an NT code, HMRC may continue deducting UK tax unnecessarily.

Key points:

- You must complete Form P85 when leaving the UK or submit a Double Taxation Treaty Relief form (often DT-Individual).

- An NT code is not automatic – it must be applied for.

- If you return to the UK, your tax code will be adjusted again.

This is an important step to avoid being taxed twice and to ensure your pension is paid efficiently.

Inheritance Tax

Inheritance Tax (IHT) remains a vital consideration for UK expats, now subject to residence-based rules from April 2025.

Long-Term UK Residence Rules (Effective 6 April 2025)

From 6 April 2025, domicile is no longer determinative for IHT liabilities on worldwide assets:

- If you’re a long-term UK resident (LTR), i.e. tax resident in 10 of the preceding 20 years, your non-UK assets are within the scope of IHT.

- Leaving the UK doesn’t immediately remove this exposure. An LTR remains liable for IHT for 3–10 years after departure, depending on residency length (a “tail”).

Why This Matters for Retirement Abroad

These changes impact long-term retirement plans:

- If you were UK resident for a decade or more before retiring abroad, your overseas assets may still face IHT for years after departure.

- Strategic planning, e.g. adjusting residency timeline, restructuring assets, or gifting in advance, can mitigate exposure.

- Review your estate plan and check with professional advisers to ensure your legacy passes as intended.

Private Pensions and Lump Sums

Private pensions can be paid abroad, but taxation and drawdown options vary.

- The Pension Commencement Lump Sum (PCLS), often known as the 25% tax-free lump sum, may be taxed in your new country of residence.

- Regular pension income is often taxed where you live, depending on the Double Tax Treaty.

- Some expats explore QROPS (Qualifying Recognised Overseas Pension Schemes), but these are not suitable for everyone.

- Some UK pension providers severely restrict drawdown options for Brits living overseas.

👉 Professional advice before drawing pension benefits is essential.

Wills and Estate Planning

Writing a will is essential for anyone, but it becomes even more critical when you retire abroad.

Without one, local inheritance laws could dictate who receives your estate, sometimes in ways that conflict with your wishes.

Why Wills Matter More for Expats

- Many countries (such as France, Spain, Portugal, and Greece) have forced heirship rules. This means certain family members (such as children) are automatically entitled to part of your estate, even if your UK will says otherwise.

- If you die without a valid will in place, your assets may be subject to intestacy laws both in the UK and in your country of residence.

Do You Need Two Wills?

For many expats, the solution is to have:

- A UK will – covering UK assets such as pensions, bank accounts, and property.

- A local will – drafted in line with the laws of your country of residence, covering assets there.

These wills must be carefully drafted to work together, not contradict each other.

Professional legal advice in both jurisdictions is vital.

EU Succession Regulation (Brussels IV)

If you live in an EU country (except Ireland and Denmark), you may be able to elect for UK law to apply to your estate instead of local forced heirship rules.

This is done through your will.

💡 Example: A British expat in France can include a clause in their French will choosing UK law to govern the distribution of their estate. This allows them to leave assets more freely, rather than being bound by forced heirship.

🔗 EU Succession Regulation: What is it and how does it affect UK expats?

Practical Steps

- Review your will(s) before moving abroad.

- Consider drafting a local will in your new country.

- Update wills after major life changes (marriage, divorce, property purchase, relocation).

- Coordinate wills with wider inheritance tax planning.

Retirement readiness quiz

Savings and Investments

ISAs

ISAs lose much of their appeal once you move abroad:

- You cannot contribute once non-resident.

- Most countries do not recognise ISA tax benefits, meaning income and gains could be taxed locally.

🔗 Expat ISA Rules: What Can Be Done With an ISA When You Move Abroad?

Expat-Friendly Investment Options

- Offshore bonds – tax-deferred investments, recognised across Europe.

- Country-compliant solutions – such as French Assurance Vie or Spanish Compliant Investment Bonds.

These can provide more efficient tax and estate planning than keeping UK ISAs.

Property Abroad

Owning property abroad is a popular retirement goal, but rules vary.

- Residency rights – Property ownership may support visa applications.

- Inheritance laws – France and Spain enforce forced heirship rules.

- Taxes – Property purchase and ownership costs can be higher than expected.

- UK property – Keeping a UK home may affect tax residency status.

Residency & Visa Requirements in the EU

Post Brexit, UK citizens no longer have automatic rights to live in the EU.

- Spain – Non-Lucrative Visa requires proof of €28,800 annual income (plus €7,200 per dependant).

- Portugal – The D7 Visa requires proof of passive income or savings, with a minimum around €9,000 per year.

- France – Long Stay Visa requires income equivalent to the French minimum wage.

- Poland – Residence permits available for retirees married to Polish citizens.

Each country has different requirements – research carefully and allow plenty of time.

Healthcare Abroad

Healthcare access is one of the most important retirement issues.

- In EU countries, retirees with a UK State Pension may qualify for the S1 scheme, giving access to public healthcare.

- In other countries, or before the S1 is approved, private health insurance is often mandatory.

Healthcare costs should be factored into your retirement budget.

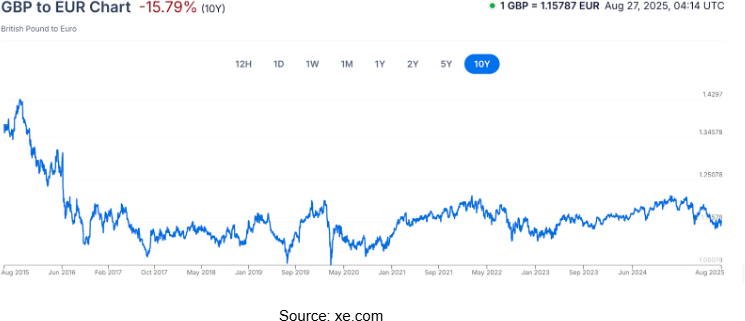

Currency & Banking

Living abroad means your income and expenses may be in different currencies.

- Exchange rate fluctuations can significantly reduce your spending power.

- Specialist currency transfer providers often offer far better rates than high street banks.

- Multi-currency accounts can help smooth transfers and give flexibility.

Practical Lifestyle Considerations

Finances are important, but so is quality of life.

- Language – Will you learn the local language, or live in an expat community?

- Community – Spain, Portugal, and France have large British expat networks, while Poland and Greece are smaller.

- Climate – Hot summers or cold winters can be challenging.

- Family – Consider how often you’ll travel back to the UK for family events.

Case Study: Kevin & Sally’s Retirement in Spain

Kevin and Sally, both aged 62, had been dreaming of retiring to Spain for years.

With holidays to the Costa del Sol behind them and a second home already in Malaga, the decision to move permanently once they stopped working seemed like the perfect next step.

But as they soon discovered, moving abroad for retirement came with a series of financial, legal, and lifestyle challenges that required careful planning.

Challenge 1: Understanding UK State Pension Rules

Both Kevin and Sally had built up strong UK National Insurance records and were on track for the full UK State Pension.

The issue: Would Brexit or moving to Spain mean a frozen pension?

The solution: Because Spain is in the EU, their State Pension continues to increase annually under the UK’s triple lock system.

They also checked their National Insurance record through gov.uk and topped up a few missing years with voluntary contributions to secure their maximum entitlement.

Challenge 2: Private Pensions and the Lump Sum

Kevin had a large defined-contribution pension, while Sally had two smaller workplace pensions.

They were both looking forward to taking the 25% tax-free lump sum (PCLS) to fund some renovations on their Spanish villa.

The issue: Would the lump sum still be tax-free in Spain?

The solution: Advice confirmed that while the PCLS is tax-free in the UK, Spain does not recognise it as such.

By taking their PCLS before leaving the UK, they ensured it was received free of UK tax, then moved abroad with the cash already in hand.

Their ongoing pension income would then be taxed in Spain under the UK–Spain Double Tax Treaty, rather than in the UK.

Challenge 3: Tax Residency and Double Taxation

Kevin and Sally were concerned about becoming Spanish tax residents and what that meant for their income.

The issue: Would they be taxed in both the UK and Spain?

The solution: They registered with the Spanish tax authorities and applied for an NT (No Tax) code from HMRC, ensuring their UK pensions were paid gross. Going forward, their pensions would be taxed only in Spain.

They also received advice on the Statutory Residence Test, ensuring they met the criteria to be classed as non-UK tax residents.

Challenge 4: ISAs and Investments

Both Kevin and Sally had built up substantial ISA portfolios in the UK.

The issue: While ISAs are tax-free in the UK, Spain does not recognise the ISA wrapper.

This meant that once resident in Spain, income and gains from their ISAs would become fully taxable under Spanish law.

The solution: Before leaving the UK, Kevin and Sally sold their ISA assets, realising the gains while they were still UK residents, ensuring they were completely free of UK Capital Gains Tax.

They then reinvested the proceeds into a Spanish Compliant Investment Bond, which offered:

- Tax deferral – no annual taxation on growth, unlike direct investments.

- Favourable withdrawal treatment – only a portion of each withdrawal is treated as taxable income in Spain.

- Estate planning benefits – ability to nominate beneficiaries and reduce succession complexities.

- Simplified reporting – bonds are recognised by the Spanish tax authorities, making compliance straightforward.

This gave them a tax-efficient, long-term investment structure suitable for their new life in Spain.

Challenge 5: Wills and Inheritance

Kevin and Sally already had a UK will, but they were unaware that Spanish inheritance law is governed by forced heirship, which could mean their children automatically inherit a portion of their estate, regardless of their wishes.

The issue: Their UK will alone would not guarantee that their assets in Spain were distributed according to their wishes.

The solution: They created a Spanish will alongside their UK will, ensuring both were coordinated. Importantly, they included a clause under the EU Succession Regulation (Brussels IV) electing for UK law to govern their estate. This gave them the freedom to leave their Spanish property and assets in the way they wanted.

Challenge 6: Currency and Banking

Their pensions would still be paid in pounds sterling, while their day-to-day spending was in euros.

The issue: Exchange rate fluctuations could have a big impact on their monthly income.

The solution: They opened a multi-currency account and arranged to transfer pensions into euros each month using a specialist FX provider instead of their UK bank. This reduced fees and gave them better control over exchange rates.

Challenge 7: Lifestyle Adjustment

Moving from a busy UK city to Malaga brought practical and emotional challenges too.

The issue: How to integrate into the local community and avoid isolation?

The solution: Kevin and Sally took Spanish language classes, joined a local cycling group, and connected with both British expat and Spanish neighbours. They now enjoy a balance of local integration and expat support.

Outcome

- A secure retirement income – with State and private pensions paid efficiently into Spain.

- Tax-efficient investments through a Spanish Compliant Investment Bond.

- Peace of mind with wills and inheritance planning aligned across the UK and Spain.

- A comfortable lifestyle in Malaga, with reduced living costs and a vibrant social circle.

💡 Be like Kevin and Sally – Schedule a free introductory call to discuss your overseas retirement plans

Thinking of Retiring Overseas?

Download my FREE checklist

Make your move stress‑free with our free Retiring Overseas Checklist. Clear steps, no fluff – just what you need to plan with confidence.

FAQ: Retiring Abroad from the UK

Can I still collect my UK State Pension if I retire abroad?

Yes. The State Pension is payable worldwide. However, it will only increase annually if you live in the EU/EEA, Switzerland, or a country with a reciprocal agreement. In countries such as Canada, Australia, and New Zealand, your pension will be frozen at the rate you first claim it.

Do I still pay UK tax if I live abroad?

Not usually. Once you’re non-resident under the Statutory Residence Test, you’ll typically pay tax in your country of residence instead. Double Tax Treaties (DTTs) help ensure you don’t pay tax twice.

What is a No Tax (NT) code, and do I need one?

If you become non-resident, you can apply to HMRC for an NT code. This allows your UK pension (and sometimes other UK income) to be paid gross (without UK tax deducted at source), leaving taxation to your new country of residence under the DTT.

Can I keep my ISA if I move abroad?

Yes, but you cannot contribute further once non-resident. Many countries do not recognise ISA tax advantages, so income and gains may be taxable locally. Expats often switch to tax-efficient international investment solutions.

Will my pension lump sum (25% PCLS) be tax-free abroad?

Not always. While it’s tax-free in the UK, many countries treat it as taxable income. Always check local tax rules before drawing your lump sum.

Do I need private health insurance abroad?

Yes, in most cases. If you’re moving to an EU country and receive a UK State Pension, you may qualify for the S1 scheme, which grants access to state healthcare. Otherwise, you’ll usually need private health insurance, especially when applying for residency.

Should I sell my UK home before retiring abroad?

It depends. Keeping a UK home may affect your tax residency and expose you to UK property taxes. On the other hand, selling can simplify your finances and help fund retirement abroad. Professional advice is essential here.

How do inheritance tax rules affect me if I live abroad?

From April 2025, domicile rules were replaced by long-term UK residence rules. If you’ve lived in the UK for 10 of the past 20 years, your worldwide estate remains subject to UK Inheritance Tax. Even after leaving, you may remain within scope for 3–10 years depending on how long you were UK resident. Local inheritance and succession laws will also apply.

Do I need a new will if I retire abroad?

Yes, in most cases. You should usually have a UK will for UK assets and a local will for assets in your country of residence. In EU countries, you may be able to elect for UK law to apply to your estate under the EU Succession Regulation (Brussels IV).

What are the biggest mistakes UK retirees make when moving abroad?

❌ Assuming ISAs remain tax-free

❌ Not applying for an NT code, leading to double taxation

❌ Forgetting pensions may be frozen in certain countries

❌ Underestimating healthcare costs

❌ Failing to update wills and estate planning for local law

❌ Ignoring currency risk on pension income

Useful Resources

💡 Claiming State Pension if you retire abroad

💡 Tell the taxman you are leaving (P85)

Final Thoughts

Retiring abroad from the UK can be the adventure of a lifetime.

From sunny Spain to historic France, from Portugal’s relaxed pace of life to Poland’s affordable living, the opportunities are endless.

But success lies in preparation.

By addressing pensions, tax, property, healthcare, and lifestyle issues in advance, you’ll set yourself up for a secure and fulfilling retirement overseas.

👉 Explore my detailed guides to popular destinations:

🇪🇸 Retiring to Spain from the UK

🇵🇹 Retiring to Portugal from the UK (coming soon)

🇫🇷 Retiring to France from the UK (coming soon)

🇬🇷 Retiring to Greece from the UK

🇵🇱 Retiring to Poland from the UK

🇦🇪 Retiring to Dubai from the UK (coming soon)

Talk to an Expert

Retiring abroad has never been more popular — but for British expats, the financial implications can be complex. Tax residency, healthcare, pensions, currency, local tax rules, estate planning and long-term income strategy all need to align for a smooth retirement overseas.

I’m Ross Naylor, a UK-qualified Chartered Financial Planner and Pension Transfer Specialist with almost 30 years’ experience helping people retire abroad confidently, whether they’re moving to Europe, the Middle East, Asia or back and forth between countries.

I firmly believe your location in the world should never be a barrier to expert, impartial and transparent financial advice you can trust.

Whether you’re unsure how your UK pensions will be taxed abroad, how to structure income in a new currency, what happens to ISAs, how to avoid double taxation, or how to plan for UK Inheritance Tax while living overseas, I’ll help you build a fully coordinated retirement plan that works across borders — not just in the UK.

Book a confidential consultation